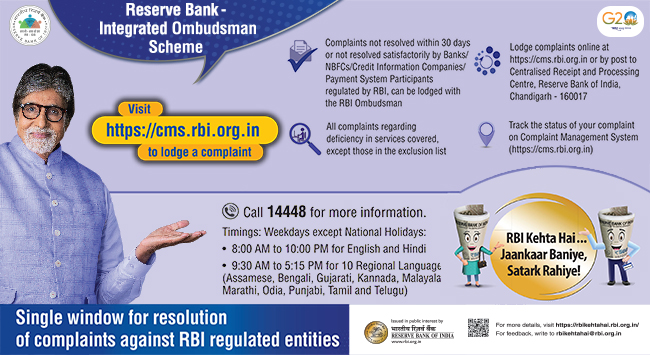

Lodge a Complaint

Give a Missed Call to 7799022129 to fetch your CKYC Card.

Important Announcement

Honours Your Trust

Apply Now

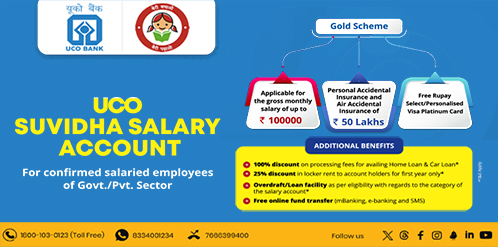

A savings account has now become a financial instrument that helps you secure your funds.

- UCO Suvidha Salary Account (UCSSA)

- UCO Saral Savings Deposit Scheme

- No-Frills Savings Bank Account (Zero Balance)

Buying a home is one of the most important financial decision you and your family will ever make.

- UCO Home

- UCO Pre Approved Home Loan

- UCO Top - Up Home Loan

UCO Rupay Personalised Debit Cards

- Daily Limit ATM : Rs 50,000/- & POS/E-Commerce- Rs 1,00,000/-.

- One time Domestic Lounge access free per quarter per card.

- Contactless Payment.

Exciting offers and Trending Deals

- Handpicked exclusive offers

- Plutos one shopping Deal offer

- UCO Bank Rupay Card Festive offer

- UCO Bank Rewardz - Earn U-Coins

Video Gallery

-

This is a pre-recorded video. Captions and audio descriptions are available.

-

This is a pre-recorded video. Captions and audio descriptions are available.

-

This is an embedded YouTube video.

-

This is an embedded YouTube video.

New Launch

Important Links

- Follow us on

-

-

-

-

-

-